For high-net-worth real estate investors, building wealth hinges on liquidity, borrowing power, and control. With more certainty after the passage of Trump’s One Big Beautiful Bill, many clients are seeking the best way to plan for future tax liabilities while remaining flexible with their assets for continued growth.

Estate planning often involves transferring assets to irrevocable trusts to shield against creditor risk, asset appreciation, and estate taxes. While we utilize gifting strategies and understand their effectiveness, real estate investors must understand the implications of these transfers to maintain flexibility and control for future expansion. Although estate taxes can burden illiquid portfolios, potentially forcing heirs to sell properties to cover taxes, clients should carefully evaluate all planning options to balance the growth of wealth along with tax ramifications and creditor protection.

Common themes with the majority of our real estate clientele:

- Leveraged Assets with personal guarantees

- Contingent liabilities with bank debt

- Assets positioned for growth

- Illiquid balance sheets

- 1031 exchanges

This is where we discuss the benefits of liquidity and utilizing the power of properly structured, trust-owned life insurance to protect against unforeseen liabilities and tax exposure. The tax-free benefits of permanent life insurance allow our clients to hedge against risk, preserve ownership of properties, maintain traditional lending relationships, and continue operational control.

Lenders May Be Reluctant to Lend to Irrevocable Trusts

- Limited Recourse: Lenders prefer borrowers whom they can pursue personally if needed. Trust-Owned property typically shields beneficiaries and grantors from personal liability, making recovery riskier for lenders in the event of a default.

- Complexity and Legal Uncertainty: Every irrevocable trust is unique. Lenders must analyze the trust agreement to verify trustee powers, limitations, and rights to encumber property. This adds legal complexity and underwriting burden.

- Challenges with Specialized Lenders: Although there are specialized lenders who will lend to irrevocable trusts, they often view these trusts as less favorable borrowers due to complicated trust agreements and restricted control over assets. As a result, credit terms are often less favorable: lower loan-to-value (LTV) ratios, higher interest rates, and tighter covenants compared to loans secured by personally or LLC-owned property.

For investors focused on growth, moving assets out of your estate can be premature. If you’re still looking to expand your portfolio, you need flexibility to borrow and leverage your properties to fuel expansion.

The Proper Use of Trust-Owned Life Insurance Can Hedge Risk

In many situations, trust-owned life insurance can allow real estate investors to create liquidity to hedge against liabilities and can deliver critical

benefits:

- Liquidity to Pay Off Debt: The policy’s tax-free death benefit can allow the surviving spouse to pay off debt, thereby eliminating the need to sell assets.

- Cash for Partners to Buy Out Surviving Spouse’s Interest: Oftentimes, the ownership of the policy can be structured in such a way that the deceased’s partner can utilize tax-free death benefit proceeds to buy out the surviving spouse’s interest in real estate companies.

- Liquidity for Estate Taxes Without Selling Properties: The tax-free death benefit provides immediate funds to cover estate tax liabilities upon the second spouse’s death, eliminating the need to sell properties while preserving portfolio continuity.

- Step-Up in Basis of Assets: Retaining ownership of real estate in personally owned entities allows for a step-up in basis upon the death of the owner, thereby significantly reducing capital gains taxes for heirs.

Why Our Clients Utilize Premium Financed Life Insurance

- Collateral Efficiency: Premium financing leverages existing assets as collateral without liquidating them, preserving their income, appreciation, and debt-servicing capacity.

- Capital Preservation: Investors secure significant death benefit coverage with minimal out-of-pocket interest payments, preserving capital for property acquisitions or improvements.

- Maximum Borrowing and Leverage Flexibility: Borrowers maintain full control to collateralize, refinance, or sell assets. They also have the ability to personally guarantee loans, resulting in better financing terms and greater capacity to leverage existing equity to fund new acquisitions or investments.

- Retained Asset Control: Investors maintain full control over properties held in their name or operating entities, while the life insurance policy can be owned by an irrevocable trust, keeping death benefit proceeds outside of the taxable estate of the borrower.

One Client’s Solution to Protect His Growing Real-Estate Portfolio

- Client in mid-40s with a $100 million net worth and a $90 million real estate portfolio, consisting of multiple LLCs and limited partnerships with $25 million in contingent liabilities.

- There were risks that Client’s debt would pass to the spouse upon death, and the spouse is not involved in the day-to-day operations of the real estate company, while also possibly facing a $28MM estate tax bill if both spouses were to pass away.

- Client was looking at utilizing his lifetime gift tax exemptions and moving his properties into an irrevocable trust, which could limit his control and financing options with lenders for future borrowing and growth of his real estate portfolio.

- CBJ Financial worked with the client’s attorney, utilizing a small portion of his lifetime exemptions to transfer an income-producing real estate asset into a Spousal Lifetime Access Trust (“SLAT”). CBJ structured a $30MM permanent policy owned by the SLAT to hedge against unexpected death and provide liquidity for debts and future estate taxes.

- The policy was financed with a customized loan collateralized by $1.5MM of clients’ unencumbered properties.

- Instead of paying hefty premiums to secure the coverage, the client paid minimal interest payments to the bank through income from the real estate asset in the SLAT, and utilized a standby Letter of Credit against an existing real estate asset to fully secure the loan.

- This strategy allowed the client to keep his companies and partnerships intact while maintaining positive relationships and favorable financing terms with existing lenders.

By leveraging trust-owned life insurance with premium financing, our client preserved capital to grow his real estate portfolio

while securing liquidity to address any debt concerns and future tax obligations

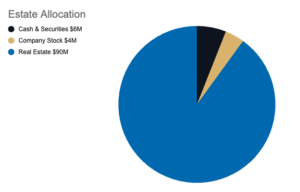

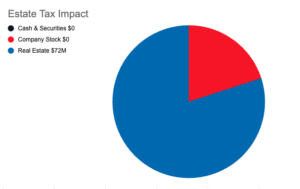

Estate Tax Implications

The chart highlights the impact of estate taxes on a $100 million estate. Upon the second spouse’s passing, the estate faces a $28 million tax bill, requiring the executor to pay the IRS in cash within a nine-month window. Oftentimes, the Executor utilizes liquid assets such as cash and securities to pay the tax. This doesn’t take into account capital gains tax on any realized gains from the sale of real estate. This accelerated timeline can present substantial difficulties, especially if market conditions force a sale at less than optimal value, potentially decreasing the estate’s worth.

Estate Allocation

Estate Tax Impact

The information provided in this article is for educational and informational purposes only and should not be construed as legal, tax, or financial advice. Tax laws and regulations change frequently and can vary based on individual circumstances. Readers should consult with a qualified tax professional, accountant, or attorney before making decisions or taking action based on the content of this article. The author and publisher assume no responsibility or liability for any errors or omissions, or for any actions taken based on the information provided herein.